Healthcare payments plumbing - Part 3

Healthcare consumerism from black friday to surgery saturday

In Healthcare payments plumbing - part 1, we covered administrative transactions that take place between payers and providers. In part 2, we looked at financial transactions - the stuff that needs to be in place for money to change hands from payers to providers. In part 3, we will cover consumer interactions - rising out of pocket costs driven by cost shifting to patients and its impact on providers, payers, and patients.

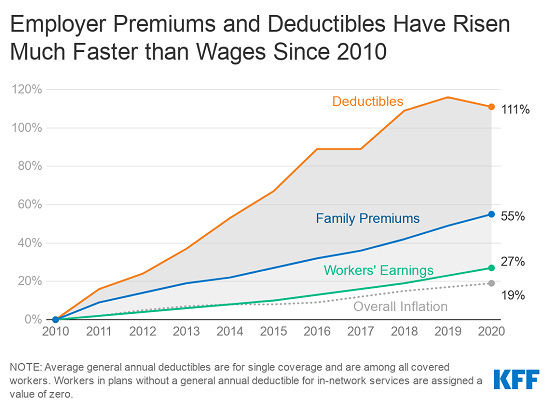

10% of all healthcare expenses in the US are paid by patients as out of pocket costs. In 2020, “out of pocket” costs like deductibles, copays, and coinsurance amounted to just under $400 billion. The payments plumbing for healthcare is undergoing a fundamental shift. Many of the quirks of US healthcare are driven by the third party payer system. Health insurers and employers have traditionally been the payers of private healthcare. They have provided payment assurance to providers. As healthcare costs have grown unsustainably, traditional payers have shifted costs to patients by way of higher deductibles (the amount patients pay before the health plan begins to pay anything), co-insurance (a percentage share of costs paid by patients when they get care) and co-pays (fixed flat fee dollar amount paid by patients when they get care). Over the last 10 years, there has been rapid growth in high deductible health plans or HDHP (plans with a deductible of at least $1,400 for individuals and $2,800 for family) - see charts below. The basic idea is that traditional payers can shift costs towards patients in exchange for lower monthly premiums. By making patients pay out of pocket, the hope is that patients become more cost conscious about their healthcare choices which will lead to a reduction in overall healthcare costs. However, there is plenty of debate whether that will actually happen - even small amounts of cost shifting leads to patients delaying care which may ultimately cost the system more. But that is for another post. Providers have traditionally relied on insurers for payment assurance. In this new dynamic, providers have to rely on unpredictable consumers for payment. This shift in the payer has significant ramifications on the revenue cycle for providers. As healthcare costs shift to patients, there is less payment certainly for providers and there is a need for new financial plumbing. Patients need new ways to save for unexpected healthcare costs, they need consumer grade payment experiences that are more inline with their expectations in other consumer settings and they need new ways to finance their expenses when they don’t have the means to pay.

Impact on providers

Providers face a different dilemma. The lack of robust payment plumbing for patients hurts providers as well. There is payment uncertainty and providers don’t know who is responsible for what at the point of service. Chasing after unpaid bills is operationally taxing and results in higher administrative costs. There are a range of new payment models, discounts and contract terms that require providers to wait for claim adjudication before pursuing copay and coinsurance payments from patients. Provider staff also have to deal with alternative payments sources and new vendors. With higher deductibles, a large portion of the provider’s revenue comes directly from the patient. Patient payments are a rising part of overall accounts receivables that may never be paid by patients. Large patient balances due to self-pay, co-insurance and high deductibles has the potential to threatens their financial stability and is often cited as a major challenge by provider organizations.

Consumer Perspective

With the background above, it is worth breaking down healthcare payments plumbing for patients in 3 buckets - savings experience, transaction experience, and financing experience. As patients become consumers and payers of healthcare, new products designed specifically for them will become an essential part of the healthcare ecosystem.

Savings experience

You can always store cash under the mattress or in a regular savings account. It’s hard to save up for healthcare when you don’t know when you would use the money or how much you would need to save. But there are tax advantaged accounts specifically designed to pay for qualified medical, prescription, dental and vision expenses that can support out of pocket medical expenses. These are not all savings accounts but they do provide a dedicated source of funding for patients. Here are the three main types.

Health Savings Account (HSA)

An HSA is basically a bank account that is only available with high deductible health plans. Employers and employees can contribute money. HSA’s have a triple tax benefit. The deposits are tax-deductible, growth in investments is tax-deferred, and spending for healthcare expenses is tax-free.

Health Reimbursement Arrangement (HRA)

An HRA is kind of like a bonus, it's set up and funded by the employer to help pay for eligible health care expenses like copays, deductibles etc. They are often coupled with high deductible health plans. Employees are only reimbursed when they submit proof of qualifying medical expenses. Employees don’t pay taxes on it and the unused funds are carried over by the employer.

Flexible Spending Account (FSA)

An FSA is an option for low deductible health plans. Employers and employees can contribute money. The deposits are tax deductible. But you cannot invest the money in this account and you can only spend it on healthcare. If you don’t spend all your money by the end of the year - it’s gone.

These models provide a financial cushion for out-of-pocket medical expenses using tax-free money. Enrollment in these types of accounts is growing but there is still a huge opportunity to drive adoption and education. Only about 17% of Americans have an HSA. There are about 30M HSA accounts holding $100 billion in assets and covering 60M people but only 7% of the accounts have some of their money invested in mutual funds. Only about 13% of Americans currently have a FSA account. There are about 460,000 FSA accounts and workers lose over $1 billion every year and employers get to keep it. New rules under the Trump administration expanded the use of HRAs to fund premiums for their employees on the individual markets which could have significant implications on benefits offered by small businesses. The trend of shifting costs towards employees will continue. However, the existing crop of products to manage out of pocket costs are badly designed. There is a huge opportunity to create new consumer friendly financial products that allow consumers to save, invest and track healthcare expenses. These new products can design creative ways to motivate consumers to shop for care and incentivize them through rewards. This type of stuff didn’t matter when insurance paid for most of healthcare. But now, with high deductibles, patients pay out of pocket and this stuff really matters.

Transaction experience

Providers can ask for payment information at the point of service or after service has been provided. However, providers have struggled to provide accurate payer and member responsibilities at the point of service because of a wide range of reasons from slow processing of claims to compliance and regulatory issues to involvement of multiple parties in establishing discounts and payers (The recent No Surprises Act is a great step forward and requires providers to furnish a good faith estimate accurate within $400) All this means that payers have to rely on patients to pay their bills after services have been rendered. That's why you get a bill after several months. But even when you get a bill, it comes via regular mail. The bill is complex and many providers can only accept checks or have very poorly designed online payment portals. The entire transaction experience for the patient is unnecessarily difficult and leads to delayed payments.

If patients are expected to pay as consumers, patients will expect the same payment experiences they have in the rest of the economy. Bills need to be easier to understand, emails need to be easier to read and logging into a portal must be a frustration free experience. Check out the survey responses below from consumers about their own transaction expectations - patients want digital communications, and online payments with a majority preferring payment by cards.

There are new startups building in this space to create easier to navigate front end user experiences but those front end tools will only be adopted by providers if they seamlessly integrate into the rest of the billing and revenue cycle infrastructure. If these same tools generate into the patient engagement experience, they will create a richer consumer grade patient experience. Lots of new players have popped up in this space target small independent providers as well as large enterprise health systems. These tools will need to provide an end to end patient experience from eligibility to patient scheduling, appointment reminders, access to health records, billing and integrations to financing options to the actual payment experience via cards or HSAs or other digital payments methods to create a seamless consumer experience.

Financing experience

Out of pocket costs do not include health insurance premium contributions. When you include premiums, US households actually pay 26% of all healthcare expenses. Households spend just over $1 trillion and are the second largest sponsors of healthcare expenses after the federal government. According to a 2020 RAND corporation study, US households pay anywhere between 16% to 33% of their income on healthcare. Even with insurance, many Americans find healthcare unaffordable and unsustainable. An HDHP’s total yearly out-of-pocket expenses (including deductibles, copayments, and coinsurance) for in-network care can’t be more than $7,050 for an individual or $14,100 for a family. People don’t have that kind of money lying around for unexpected healthcare expenses.

A third of all covered US workers are on high deductible healthcare plans. By some estimates, only 10% actually hit their deductible. This means that almost 100M people pay for every single healthcare cost. The rise in medical debt in America has also had striking parallels with the rise in high deductible healthcare plans. Almost 100M Americans also have medical debt. The total medical debt is at least $195B. 62% of bankruptcies are related to medical costs. Imagine any other market of 100M people - if basic economic forces were at work, the supply and demand of healthcare services would balance prices. However, a third party price setting system means that 100M people are at the mercy of inflated prices set by incumbent stakeholders with a goal to maximize revenue. Is it any surprise that those people have medical debt especially when they had no idea what it would cost before they got care. And when Americans have to finance their healthcare expenses the choices available to them are terrible. Lets take a look at the options.

Medical Loans and Payment Plans

Medical loans used specifically for medical costs and are available from traditional banks and online lenders unsecured (for good credit) or with collateral. Interest rates can go up to 35%. In acute care scenarios, where care is already delivered providers will set up generous no-interest payment plans, with no credit check to make sure that patients pay off their medical bill. Since the service is already delivered, the risk to collect is held by the provider. Things get more complicated with elective procedures like LASIK surgery, weight management surgeries, orthopedic, skin or fertility treatments. Providers don’t offer upfront payment plans and patients will have to apply for financing with a third party like CareCredit, which offers financing options for medical care. It is one of the largest players in the space. CareCredit offers a short term financing options via a medical credit card with a 0% interest financing for 6-24 months. However, if the balance isn’t paid back completely, patients will owe 27% interest rate on the entire amount borrowed not just the remaining balance. Longer term loans with lower interest rates are offered by CareCredit as well as other newer entrants. The high interest rates on the entire borrowed amounts comes as a surprise to many and has led to a bad reputation for these types of medical loans.

Consumer Credit Cards

Many people resort to the the easiest source of funding they have available - their existing credit cards. However, tax advantages and other credit protection of healthcare spending are non existent when the healthcare bills get bundled in with consumer credit. General purpose consumer credit cards with balance transfer, 0% interest rates also exist and might be better financing choices than medical credit cards in some cases, but it gets harder to qualify for them with poor credit scores. In general, patients should look at theses financing options as the last resort. One silver lining is that the three major credit-rating agencies recently agreed that unpaid medical bills will not affect people’s credit scores for a year. Once a bill is paid, it should come off your credit report immediately. Starting in 2023, unpaid medical debt under $500 should not appear on reports either.

Charity Care

Many patients are unaware that they may be eligible for charity care or financial assistance which could dramatically lower their medical bills. More than 50% of US hospitals are non-profits that benefit from tax exempt status. To maintain their tax exempt status, they need to offer charity care and financial assistance programs for low and middle income patients. Hospitals run their own programs and decide who is eligible based on patient’s income, household size, the bill’s age, patient’s insurance status, county or state residency, and the dollar value of the bill. One in three hospitals required patients to have incomes at or below 200 percent of the FPL ($50,200 for a family of four in that year) to be eligible for charity care. Some states have their own regulations that mandate who is eligible for charity care. New organizations (ex: Dollar For) have sprung up recently to help patients apply for charity care.

Crowdfunding

GoFundMe also calls itself the “leader in online medical fundraising,” and hosts more than 250,000 yearly medical fundraisers that yield more than $650 million each year. A third of all campaigns on the platform are for medical fundraising. But most GoFundMe campaigns fail and only 12 % reach their goals. It is also a reflection of a completely broken healthcare system when patients have to market their healthcare struggles and resort to macabre storytelling to pay for care.

Buy Now Pay Later

When I started writing about healthcare payments, I was mainly curious about healthtech - fintech business models that I have seen emerge over the last few years. Buy Now Pay Later (BNPL) models have rapidly spread in consumer e-commerce giving rise to new fintech unicorns like Affirm. The idea is simple - provide short-term, zero-interest financing by splitting payments for consumers and charging merchants instead. The low friction financing option increases demand, and merchants are willing to pay the 2-4% fee. New startups like Walnut, Nibble, Paytient have emerged that are trying to deploy this model in healthcare. These new models target patients, providers, employers, and insurers with unique value propositions. I expect a lot of innovation to happen in this space in the next few years. We will see the rise of consumer-directed healthcare powered by smooth fintech experiences that might one day drive the unbundling of traditional health insurance. Here’s how these new health tech-fintech startups are positioning themselves to stakeholders.

Spread out payments for Patients

BNPL is primarily designed to help patients spread their payments without predatory interest rates as an alternative to consumer credit cards. The default risk for healthcare payments is typically lower than other consumer credit. Some offerings will negotiate on behalf of patients and then charge a percentage of savings.

Shorten time to collect for Providers

The model also provides payment assurance because providers are paid off, and the risk to collect is offloaded. Many offerings also help shorten the time to manage accounts receivable by building consumer-friendly user experiences through credit cards and well-designed payment portals, texts, and apps that are part of everyday consumer experiences to encourage timely payments. Instead of charging patients, the business models are aimed at collecting fees from providers, who are willing to offer discounts and/or pay fees for driving patient collections.

New benefit offering from Employers

An interesting strategy is positioning this offering as an employee benefit. The business model is based on charging per employee/member fees from employers who are willing to include these products as a part of the benefits package. Embedding the product within the employer benefits package also allows these companies to tap into payroll deductions for payments, further reducing risk and providing tax advantages for healthcare payments while offering zero-interest, zero-fee financing.

Offering innovative models to modern health plans

Finally, there is also an opportunity to position the model to take advantage of a changing payer mix. Cash pay discounts can lead to lower out-of-pocket costs for patients than going through insurance and paying down a deductible or coinsurance for a negotiated rate. These financial products are positioned to help beneficiaries to find in-network or out-of-network care at a lower out-of-pocket cost and allow them to still pay directly but get reimbursement from their insurance or have costs count towards the deductible.

That’s it! Healthcare payments are way more complex than 3 posts can cover, and we obviously haven’t gone as deep as we could go. This space is rapidly changing. Price transparency regulation and the availability of a net new data source will power entirely new healthcare payment experiences for payers, providers, and patients over the next 5 years.

Do you work in the payments space? Do you know this stuff really well? Reach out or comment below and share where I got things right and where I got them wrong. Always open to feedback!

Thanks for reading hick-picks! If you enjoyed reading, please like, comment, share and subscribe. Find me on LinkedIn, Twitter, tejasinamdar.com

Awesome post!

Selfishly going to plug Flexpa here if that's okay, since it's seemingly relevant - as a digital mechanism to synchronize claims as soon as they are adjudicated, medical bill pay applications can more easily help their patients - offering financial assistance as soon as patient costs are surfaced.